Many people, including self-employed persons and employers, might not be aware of the troublesome rules of benefits of kind. Sometimes it may be tricky to understand them as few of them are taxable and few aren’t. Due to the complex rules, it may be difficult to know which rules apply as per your situation.

But you don’t need to worry, as this quick guide will help you learn what are benefits in kind, which BIKs are taxable and which aren’t, how to report and pay BIK and why you need to maintain proper records of them. Note that is guide is just for the basic information on BIKs and doesn’t serve as a definitive guide.

We recommend you consult a professional accountant in this regard. Contact us right now!

Understanding Benefits in Kind

Benefits in Kind are non-cash benefits- also referred to as fringe benefits and perks- provided to employees or directors of the company other than their wages or salary. These benefits can be in form of assets like vehicles, or services, like private healthcare, etc. Most of the benefits that have any monetary value are known as a benefits in kind.

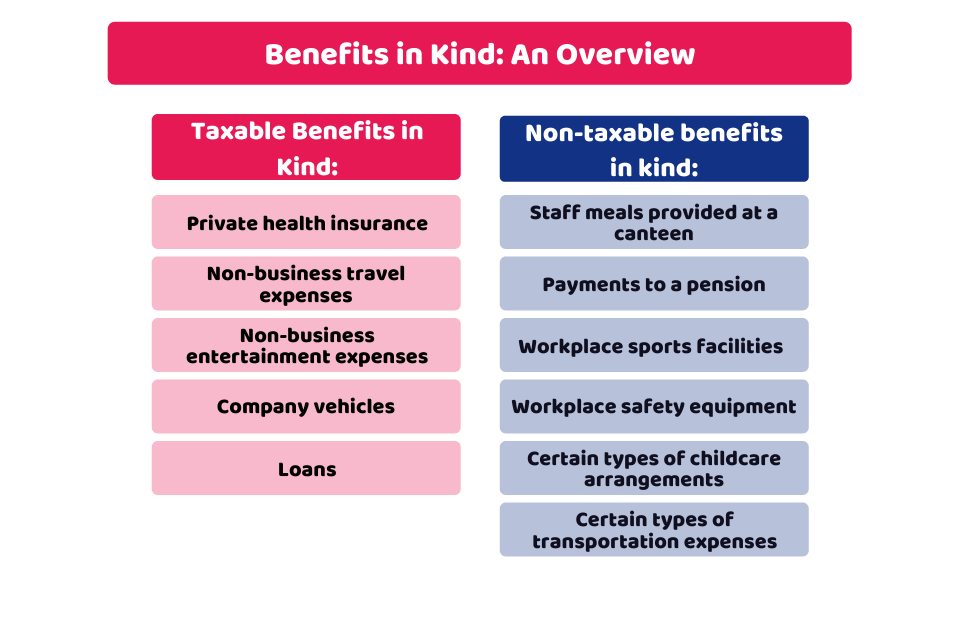

Taxable BIK

Here are some of the examples of benefits that are taxable:

- Private health insurance

- Non-business travel expenses

- Non-business entertainment expenses

- Company vehicles

- Loans

Non-Taxable BIK

Non-taxable benefits include:

- Staff meals provided at a canteen

- Payments to a pension

- Workplace sports facilities

- Workplace safety equipment

- Few types of childcare arrangements

- Few types of transportation expenses (like subsidies for public bus services)

Visit the HMRC’s resources for further information on the BIKs, and how they are treated for tax purposes. The rules related to these benefits can be complicated. As per the circumstance or context, HMRC may levy a tax charge on you.

Ways to Report Benefits in Kind

Here are the ways you can use to report BIK:

- By Submitting the P11D and P11D(b)

- HMRC’s PAYE Online service

- Payroll software

- HMRC’s Online End of Year Expenses and Benefits service

Reduce your business burden by letting us prepare & manage your company accounts! Our team of experts will provide the best solutions to all your business problems at an affordable package! So, contact us now!

How to Report and Pay tax on BIK?

Employers need to report all benefits at the year-end and need to make contributions at a rate of 13.8%. Sometimes, employees might need to pay NI on BIKs as they are considered the income of the employees. There are two ways to pay:

1) By Submitting P11D Form

The P11D keeps track of BIK that employees, including the director, receive at the year-end. Employers are required to submit a form for each employee for whom they have provided the BIKs.

Self-employed individuals are taken as both the employee and employer. In such a case, they have the responsibility for filing the P11D. You need to submit a P11D(b) for the below conditions.

The conditions for a P11D(b) submission are:

- You submitted any P11D form

- You’ve offered the employees’ benefits via your payroll

- You’ve got a reminder/notice from HMRC

P11D(b) is a form that shows the taxable benefits that an employer has provided for its employees, and indicates the amount of Class 1A National Insurance payable on benefits and expenses.

2) Paying Tax on Benefits Through your Payroll

Secondly, the employer needs to make deductions and is liable to pay tax on employee BIKs through the payroll. Registration with HMRC is required before 6th April. Bear in mind that the P11D form isn’t needed if you’re offering the benefits through your payroll, here you are required to submit the P11D(b).

Maintaining Proper Records

By maintaining proper records, it will let HMRC know that you have reported everything accurately and correctly. Then they are further reviewed by HMRC. Generally, the following records are necessary:

- Details of every benefit you’ve offered

- Information required to calculate the amounts indicated in your end-of-year forms

- The payment that your employee has contributed to a benefit

- Any communication you have with HMRC

All payroll records should be kept at least for three years from the year-end they are associated with. Oftentimes, employers keep these records for six years and they are also known as accounting records.

Quik Sum Up

So that’s all about benefits in kind. Some of them are taxable and some are tax-free. You can submit them with a P11D form or you can pay the BIK liabilities through the payroll. Note that you need to keep proper records to let HMRC review your BIK.

If you want to learn more about BIKs, or the complex tax issues surrounding them, feel free to contact us!

We’re an accounting firm in London offering affordable accounting services in the UK for limited companies, property owners, and self-employed professionals. Get in touch with us today!

Looking for a customised offer? Get an instant quote now!

Disclaimer: This blog is written for general information on BIKs.