You will have to pay taxes even after retirement. The money you will get as a pension is classed as income, and on most of the income, you must pay tax. So, it is essential to know how tax on pension works. This blog will help you how to get the most out of your retirement investments, how to minimise unnecessary losses, and how to increase your retirement income. Let’s get started!

Turn to us if you want to boost your pension income! We have a team of skilled accountants who provide accounting and taxation services at a very competitive rate. Contact us right away!

How Tax on Pension Works?

Your pension, like other income, is subject to taxation. Your tax liability depends on your total taxable income. The following are included in taxable income:

- Earnings from your self-employment or employment

- Earnings from your property

- Earnings from your savings

- Earnings from your investments

Usually, you pay tax when the value of your pension pots surpasses the limit (£1,073,100) of the lifetime allowance. Your pension provider will subtract the charge from your payment before you get it.

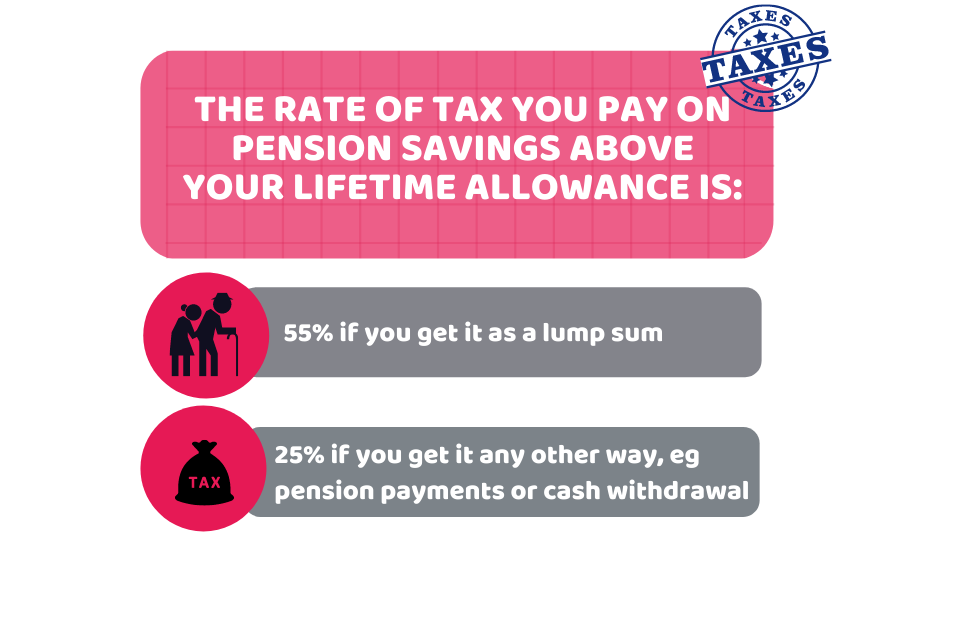

You will have to pay the following percentage of tax on pension, saving more than your lifetime allowance:

- In case you receive a lump sum, then the tax rate is 55 percent.

- In case you receive it any other way, such as through cash withdraws or pension payments, the tax rate is 25 percent.

Tired of taxation problems? Let us handle this!

How Much Your Pension Income is Tax-Free?

You do not have to pay tax on the following:

- The first of the personal allowance (£12,570) of annual total income.

- Savings income of up to £6,000 annually

- Your personal pension withdrawals up to 25 percent (the exact amount of money will depend on the withdrawal method).

Your pension tax is calculated based on your total income minus allowances. Your pension provider will deduct the tax from your income if your private pension exceeds £1,073,100. If you receive a state pension, HM Revenue & Customs will subtract it from your pension pot automatically. The remainder of your pension is taxable as usual.

How Can I Avoid Paying Pension Taxes?

The strategy to avoid paying it is to withdraw the minimum amount of income you need annually. In simple words, the minimum your income is, the less amount of tax you will pay.

Of course, you should withdraw as much income as you need to live your life comfortably. But taking out more money than required and putting it into savings is less advantageous than getting a salary. Therefore, it is recommendable to keep money inside your pension until you need it.

In addition to that, you can take benefit from the drawdown scheme too. This scheme helps you adjust your income on an annual basis, allowing you to save more money in taxes.

If you have an annuity, you won’t be able to take advantage of this flexibility because your annuity income will be the same every year. However, the drawdown scheme has a set of risks associated with it.

Conclusion

Now that you understand how tax on pension works. You have to keep in mind that you can not run from paying tax even after retirement. Therefore, go through the above-mentioned tax rates, you must pay on your pension income. But, it is more recommendable to take professional advice, as this is a complex business affair.

Allow us to reduce your business burden by handling all your tax affairs! We are friendly and cost-effective! We will solve all your taxation issues in no time! Contact us now!

Disclaimer: This blog is a basic overview of how tax on pension works.